Abstract After October, the renminbi has to help out the SDR will be going? The World Bank’s issuance of SDR debt may be just the beginning of a series of good games. Looking to the future, if properly promoted, SDR as a super-sovereign currency, worthy of expectation in the international monetary system. G20...

After October, where will the SDR with RMB help go? The World Bank’s issuance of SDR debt may be just the beginning of a series of good games. Looking to the future, if properly promoted, SDR as a super-sovereign currency, worthy of expectation in the international monetary system. The G20 Hangzhou Summit has just come to an end. On October 1, the RMB will officially join the SDR (Special Drawing Rights), which indicates that the RMB has officially become “freely usable currencyâ€.

Last week, the People's Bank of China announced that it authorized the Bank of China, New York Branch to provide RMB clearing and settlement services in the United States.

At the end of August, the World Bank's International Bank for Reconstruction and Development (IBRD) issued 500 million SDR bonds in the Chinese interbank market. The bond coupon rate was 0.49%, and the subscription multiple was 2.47. The market reaction was higher than expected.

In the declaration of the Hangzhou Summit, a special mention of the RMB and SDR was specifically mentioned: “According to the decision of the International Monetary Fund, we welcome the RMB to be included in the SDR currency basket on October 1. We support the ongoing expansion in special Research on the use of drawing rights, such as the wider distribution of financial and statistical data with SDR as reporting currency, and the issuance of special drawing rights denominated bonds to enhance resilience. In this regard, we note the recent World Bank Special drawing rights bonds were issued in the Chinese interbank market. We welcome further work by international organizations to support the development of the local currency bond market, including strengthening support for low-income countries."

The big drama about the renminbi and SDR is about to kick off. We believe that the renminbi's participation in SDR is not only symbolic. In time, if all parties can make a difference, SDR (including the interaction between RMB and SDR) will have a profound impact on the global monetary and financial system.

Why does the world need SDR?

In the 1960s, in order to solve the huge liquidity pressure faced by the Bretton Woods system, the G10 (G10) appointed a group of experts to conduct research on the new reserve currency issue in 1963. In 1965, the group first proposed the concept of CollectiveReserveUnit. The second US dollar crisis broke out in the late 1960s, prompting the IMF to formally adopt a reserve currency program in 1969 and created a special drawing right.

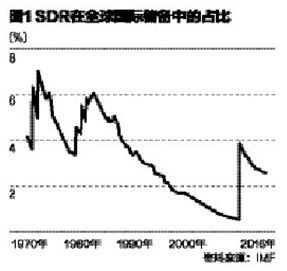

At the time of its creation, the SDR was directly linked to the US dollar. The equivalent of 1 unit SDR was $1. After the disintegration of the Bretton Woods system in 1973, the value of SDR began to be determined by a basket of currencies. SDR's basket currency initially has 16 currencies. In 1980, the IMF identified the SDR currency basket as five types – the US dollar, the British pound, the Japanese yen, the mark, and the franc. In 2001, the euro replaced the mark and the franc, and the other currencies remained unchanged. The IMF meets every five years to determine the relative weight of each currency in the SDR pricing currency basket.

The IMF announced on November 30, 2015 that the RMB will officially be added to the SDR currency basket as the fifth currency in October 2016. On September 30th, the IMF will announce the specific amount of RMB in the SDR basket composition. The SDR composition that will be officially launched will be like this (see Table 1).

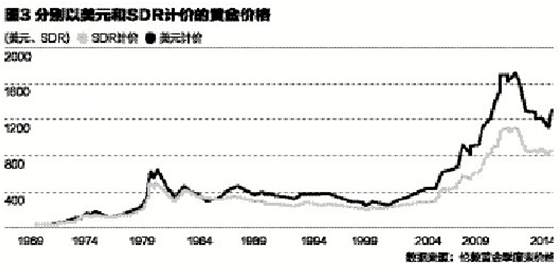

First of all, from the perspective of pricing tools, the risk dispersion principle of asset portfolio makes the stability of basket currency pricing better than single currency. If oil and gold are converted to SDR, the price change will be significantly smaller (Figure 2, Figure 3). The price standard deviation of SDR-denominated oil and gold is significantly lower than the dollar-denominated level, and the ratio of the standard deviation to the mean value of the SDR is also significantly lower than the dollar-denominated level (Table 2). In addition, the ratio of SDR to the US dollar fluctuates significantly less than other sovereign currencies.

Finally, and most importantly, SDR as an official reserve (O-SDR) has great potential to improve the global monetary and financial system. For reserve currency issuers, O-SDR helps to alleviate its burden and alleviate the dilemma caused by the Triffin problem. At the same time, the rapid growth of global foreign exchange reserves in recent decades is closely related to the Jamaican system, non-key currency countries. Have to store a certain amount of reserve assets, in order to ensure that they are as active as possible in the existing international monetary system, which in turn leads to the disorderly large flow of capital between emerging markets and developed markets, and reserve issuance If the country’s huge debts can expand the use of O-SDR and make it assume the role of international reserves on a larger scale, it will help to change the current situation of non-reserve issuers holding large amounts of foreign exchange reserves, fundamentally changing global imbalances.

How will SDR and RMB interact?

After the renminbi joins the SDR, what kind of positive interaction will happen between the two? We are full of expectations for this.

For the RMB and Chinese investors, first of all, due to the entry of SDR, the capital project is not fully open. The RMB can directly enter the global financial market through SDR, and has SDR assets, that is, RMB assets are allocated. Second, with SDR bonds, Chinese investors also have US dollar assets, which can also cross barriers that are not fully open for capital projects. Third, the renminbi's participation in the SDR currency basket has increased the international credibility and credibility of the renminbi. It further encourages central banks and sovereign wealth funds to hold renminbi-denominated assets and enhance the status of the renminbi as a reserve currency from the market mechanism. Fourth, the addition of RMB to SDR will further promote the internationalization of the RMB and join the SDR, which means that the IMF member countries will automatically form an exposure of RMB 210 billion through their SDR.

For the SDR and the international monetary system, the addition of the renminbi has significantly enhanced the representation of the SDR. The inclusion of the renminbi in the SDR currency basket has made the SDR's GDP representative more than 60% of the world's, and the export volume accounts for nearly 90% of the world's total. At the same time, the entry of the RMB into the SDR will make the international reserve system more stable. At present, the world's major international reserve currencies are the US dollar, the euro, the Japanese yen and the British pound. However, due to the financial crisis, the European debt crisis and the limitations of these countries' macro policies, the exchange rate The large fluctuations have affected the stability of the reserve currency system.

All parties are very concerned about the future value of the renminbi. We believe that in order to ensure a smooth transition of the basket, coupled with the G20's commitment to avoid competitive devaluation, China will not allow the exchange rate to fluctuate significantly. In this context, the actual downside of the RMB in the second half of the year should be limited, both economically and politically.

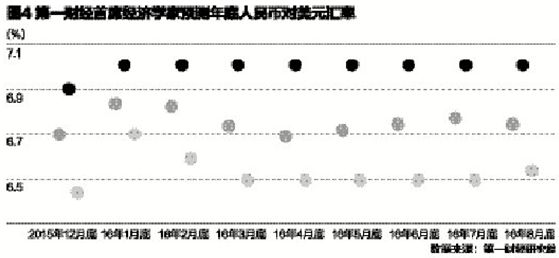

According to a survey by the chief economist of the First Financial Times, as of the end of August, economists predicted that the average exchange rate of the RMB against the US dollar at the end of the year was 6.75, which was higher than the predicted value of 6.78 in July. The forecast range was 7.00~6.55, and the future RMB depreciation Space is limited (Figure 4).

SDR future big guess

After October, where will the SDR with RMB help go? The World Bank’s issuance of SDR debt may be just the beginning of a series of good games. Looking to the future, if properly promoted, SDR as a super-sovereign currency, worthy of expectation in the international monetary system. Let us first list a list:

â— Establish a liquidation relationship between SDR and other currencies, and change the current SDR can only be used for the status of international settlement between government or international organizations, so that it can become a recognized payment means for international trade and financial transactions.

â— Promote the use of SDR as a statistical reporting currency and broaden the use of SDR in international trade, commodity pricing, securities issuance, and asset valuation. Since April 2016, the People's Bank of China has jointly used the US dollar and SDR as the reporting currency for foreign exchange reserves.

â— Further improve the valuation and distribution methods of SDR. The basket currency range of SDR valuation should be extended to the world's major economic powers, and GDP can also be considered as one of the weight considerations. The issuance of SDRs can also be changed from the artificial calculation of the value of the currency to the support of the actual assets. It can be considered to absorb the existing reserve currency of each country as its preparation for issuance.

â— Further improve the liquidity provision mechanism of SDR and establish a liquidity supplement mechanism for the SDR secondary market.

â— Actively promote the creation of SDR-valued assets, enhance their attractiveness, and form a yield curve.

â— Consider combining SDR with IMF centralized management reserves.

In each field, how far the SDR with the RMB “energy†can go will depend on the political determination and wisdom of global policy makers. Let us wait and see.

Hubei Chengze Diamod Products Co., Ltd. , https://www.ryomaltools.com